With the entry into force of FIDLEG, financial service providers will be subject to a series of rules of conduct which they must comply with when providing financial services. These rules of conduct can be divided into the following groups:

- Information obligations (Art. 8 f. FIDLEG);

- Obligation to carry out aptitude and appropriateness tests (Art. 10 et seq. FIDLEG);

- Documentation and accountability obligations (Art. 15 f. FIDLEG);

- Transparency and due diligence obligations (Art. 17 et seq. FIDLEG).

Professional clients can dispense with the observance of certain rules of conduct. The rules of conduct do not apply to institutional clients.

The FIDLEG provides for various information obligations (Art. 8 FIDLEG and Art. 9 FIDLEG) which financial service providers will have to fulfil in future before concluding contracts or providing services. In future, financial service providers will have to inform customers about their identity, their field of activity and any economic ties, among other things. The duty to provide information also includes information on the services and financial instruments offered and their risks.

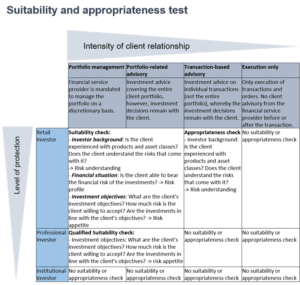

The FIDLEG provides for an aptitude and appropriateness test based on European law. A financial services provider providing investment advice or asset management services must obtain information from the client about the client’s financial situation, investment objectives and knowledge and experience of the financial services and instruments offered.

The purpose of the adequacy test pursuant to Art. 11 FIDLEG is to determine whether the client understands the risks associated with the service.

The suitability test within the meaning of Art. 12 FIDLEG serves to answer the question of whether the service is suitable for the customer in view of his willingness and ability to take risks.

The FIDLEG provides certain facilities for transactions with professional customers. It can therefore be assumed, without any indication to the contrary, that they have the necessary knowledge and experience. Furthermore, professional clients – with the exception of wealthy private individuals – can also be assumed to be able to bear the financial risks of the investment. Within the meaning of Art. 14 FIDLEG, no adequacy test is required in the context of a pure account/deposit relationship or in the case of execution-only transactions or services provided at the customer’s instigation.

The documentation and accountability obligations (Art. 15 and 16 FIDLEG) are intended to give the customer a better insight into the service provided by the financial services provider.

The financial service provider must be able to provide information to the supervisory authority at any time. As part of this documentation obligation, the financial service provider must also give reasons for its recommendation to sell or purchase financial products.

The documentation and accountability obligations (Art. 15 and 16 FIDLEG) are intended to provide customers with a better insight into the services provided by financial service providers.

The financial service provider must be able to provide information to the supervisory authority at any time. As part of this documentation obligation, the financial service provider must also document the reasons for which the purchase or sale of financial products was recommended or executed.

The documentation and accountability obligations (Art. 15 and 16 FIDLEG) are intended to give the customer a better insight into the service provided by the financial services provider.

The financial service provider must be able to provide information to the supervisory authority at any time. As part of this documentation obligation, the financial service provider must also give reasons for its recommendation to sell or purchase financial products.

The documentation and accountability obligations (Art. 15 and 16 FIDLEG) are intended to provide customers with a better insight into the services provided by financial service providers.

The financial service provider must be able to provide information to the supervisory authority at any time. As part of this documentation obligation, the financial service provider must also document the reasons for which the purchase or sale of financial products was recommended or executed.

Yes, compliance with the duties of conduct is checked by the supervisory authority and sanctions are imposed in the event of non-compliance. In addition, the FIDLEG provides for criminal liability for those persons who intentionally or negligently disregard the duties of conduct.